What are interchange fees and how do they work? Let’s have a look!

Convenient & Secure

Payment cards are the most popular, convenient, fast and secure method of cashless payments. Using them, is worth getting acquainted with the additional cost called “interchange”.

What are interchange fees?

Interchange fees are paid to card-issuing banks whenever a customer purchases with their credit/debit card. It covers the risk of a transaction’s fraud, handling costs for sending the payment to the acquiring bank and the merchant’s bank account.

Brief facts:

- Banks get interchange fees but Visa and MasterCard set the rate.

- Interchange fees were created to cover the costs of managing your card services.

- Average interchange rates may vary depending on the country.

- Debit transactions and credit card transactions are charged separately.

- Business card has a higher fee than a credit card.

- Digital transactions also carry interchange fees.

How does it work?

The interchange fee is deducted from the value of each transaction made by the Consumer with the payment card.

The profit from it goes to the bank that issued the card (e.g MasterCard or Visa) after the amount due has been collected from the acquirer, i.e. the transaction intermediary (operator of payment terminals).

Collecting the interchange fee has one main purpose – to compensate the bank for the costs of servicing the cardholder’s account.

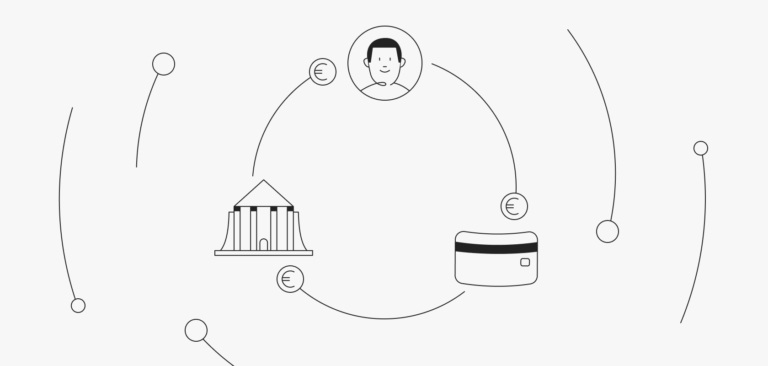

Who is paying for it?

The interchange fee is collected for a given payment card directly from the acquirer (in simple words – from the terminal operator).

However, the matter is a bit more complicated.

When the Consumer makes a purchase using a payment card, the relevant part of the funds gets charged from his account (or in the case of credit cards – from the granted limit balance).

Although, before this money goes to the merchant, it will go a long way.

In the first place, our bank will transfer the appropriate money for the purchase of goods or services to the acquirer (the operator of the payment terminal with which the consumer made the card transaction).

At this point, however, the bank will charge an interchange fee for itself.

Next, the acquirer will transfer the received funds to the merchant, i.e. the seller at the service and commercial point, but he will also keep the appropriate fees for himself and the fee for the card manufacturer.

Consequently, the seller will receive a monetary value lessened by three fees (so-called “MSC” fees).

To not lose too much on the sale itself, the merchant raises the prices of his goods.

Therefore, it can be said that the interchange fee is born by the Consumer himself – at the time of paying for chosen goods or services.

How much are interchange fees?

Interchange rates are established by the card networks. However, their rates are not static– MasterCard and Visa usually update them twice a year.

Calculation of interchange fees is rather complicated and depends on diverse components,such as:

- Card brand (e.g MasterCard, Visa etc.)

- Card type (debit, credit)

- Region of the issuer, acquirer and the merchant

- Merchant’s business type

- Transaction type

The most up-to-date way to check the current rates is to check the website of the particular payment card brand.

Below you will find interchange rates for MasterCard and Visa in the EU and US.

MasterCard interchange rates: EU,US

Visa interchange rates: EU,US

EU Interchange Fee Regulations

The final legal regulations from the EU entered into force on January 29, 2015.

As such, the current inter change rate for debit cards may be up to 0.2%, and for credit cards 0.3%.

In comparison, in the USA this amount is about 2%.

The established limits, however, do not apply to card transactions originating from a newly established card manufacturer in the first 3 years of its operation (assuming that the organization is not a partner of an already existing manufacturer, e.g.MasterCard or Visa).

Interchange++ explained

Essentially, the interchange++ model is a pricing scheme consisting of the fees charged by the card issuer, card scheme and acquirer processing a transaction.

The first“+” sign equals the costs of the payment system. This fee is usually lower than the interchange fee and ranges between 0.15% and 0.65% for e-commerce transactions.

The second“+” sign signifies the fee for processing the card service. This fee depends on the type of business, country of residence and the total turnover of the company made with the payment card.

Conclusion

Interchange rates might be a big headache for small business owners. Unfortunately, they are unavoidable for all businesses that take customer payments by debit and credit cards. However, while any processing fees are rather unwelcome, the benefits for being able to process card payments are much more profitable than the additional cost of interchange fees. So, it is not only a chance to cut some expenses but also an opportunity to make wiser data-driven decisions. All in all, it is worth mentioning that alternative payment methods also involve a processing fee. In case you pay by cash, it will be transportation and insurance costs. Newcomers are very often offering attractive processing fees or no fees at all for early adopters. Like ZEN Pay, which is free from fees for the merchant.