It should not come as a surprise that with the development of technology and the progressing digitalization of our lives, new opportunities are emerging. One of them is “Dynamic Currency Conversion”, commonly known as DCC.

In the past, exchange offices were the basic way of exchanging money for another currency. Unfortunately, this solution has its drawbacks. First of all, you need to find such an exchange office and bother to make a transaction. The exchange rate in such office, does not necessarily correspond to the real value of both currencies. It must finally earn a living. Airport exchange offices, for example, usually offer extremely unfavorable rates for customers.

It should not come as a surprise that with the development of technology and the progressing digitalization of our lives, new opportunities are emerging. One of them is “Dynamic Currency Conversion”, commonly known as DCC.

Kind of important

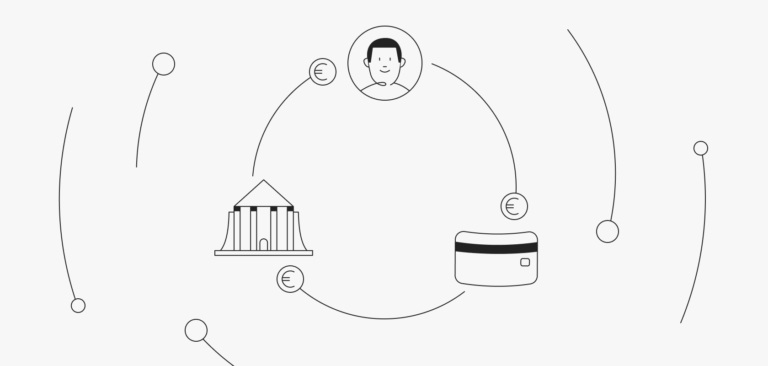

DCC services enable foreign customers with Mastercard, VISA and Diners to pay in the currency of the card. Card Organizations have implemented several specific rules regarding information that must be presented to the customer before deciding to accept or reject DCC transactions, as well as information that must be included in the customer’s confirmation.

How does DCC work?

DCC does not require your employees to know which country the card comes from. The payment terminal automatically identifies the currency. If the card is subject to a DCC transaction, the terminal will ask if the customer wants to make a non-cash payment in their native currency. Then the purchase amount will be converted to the appropriate currency based on the best exchange rate on the market and two values will appear on the screen. The terminal printout of the DCC transaction will always show the transaction in the customer native currency, the exchange rate and the amount of the transaction in the native currency of the card holder.

Increase profits with DCC

The DCC service is widely used all over the world and tourists from abroad expect it at the place where they travel. They praise it for the transparency and speed of information transfer. Nobody and nothing compels them to choose a currency. They know the final amounts that will be charged to their bills. And they avoid he additional costs of currency conversion.

What to choose abroad?

Just a few years ago, in order not to overpay for purchases and withdrawals from ATMs abroad, travelers had to have an account in the selected foreign currency. Today, multi-currency cards are already standard – one card is connected to accounts in various currencies and can handle payments in euro, dollars or pounds.

When paying abroad in a foreign currency, the bank recognizes, for example, that we pay in euros and withdraws money from an account in euros, without exposing us to additional commissions. In the case of currency cards issued in our residence country, using DCC abroad does not make sense, and may even generate additional costs associated with multiple currency conversions.

However, foreign payment systems will still offer us the DCC transaction option – after all, it is a multi-currency card, but issued in the customer country. If we accept the transaction via DCC, the system will show us the amount to be paid or withdrawn from the ATM in native currency – the first conversion. Our consent to the transaction will result in a second conversion, because our bank “knows” that we are abroad and the account in which we have the euro will be charged by default.

Set yourself up for profit

Resist your natural temptation to say “yes” just because it makes you feel comfortable. Don’t be fooled when asked if you want to complete a transaction using your home currency. Using the local currency can save you money, making your next trip abroad less expensive.