On this page

Introduction

ZEN offers more than 20 online payment methods for your goods and services, including Mastercard®, Visa, Paysafecard, PayPal, Blik, and more. You can check the full list on our website.

We wanted to make sure that our services are easy to use and fully transparent. The following sections of this document explain the basic structure and flow of the ZEN payment process.

Payment flow

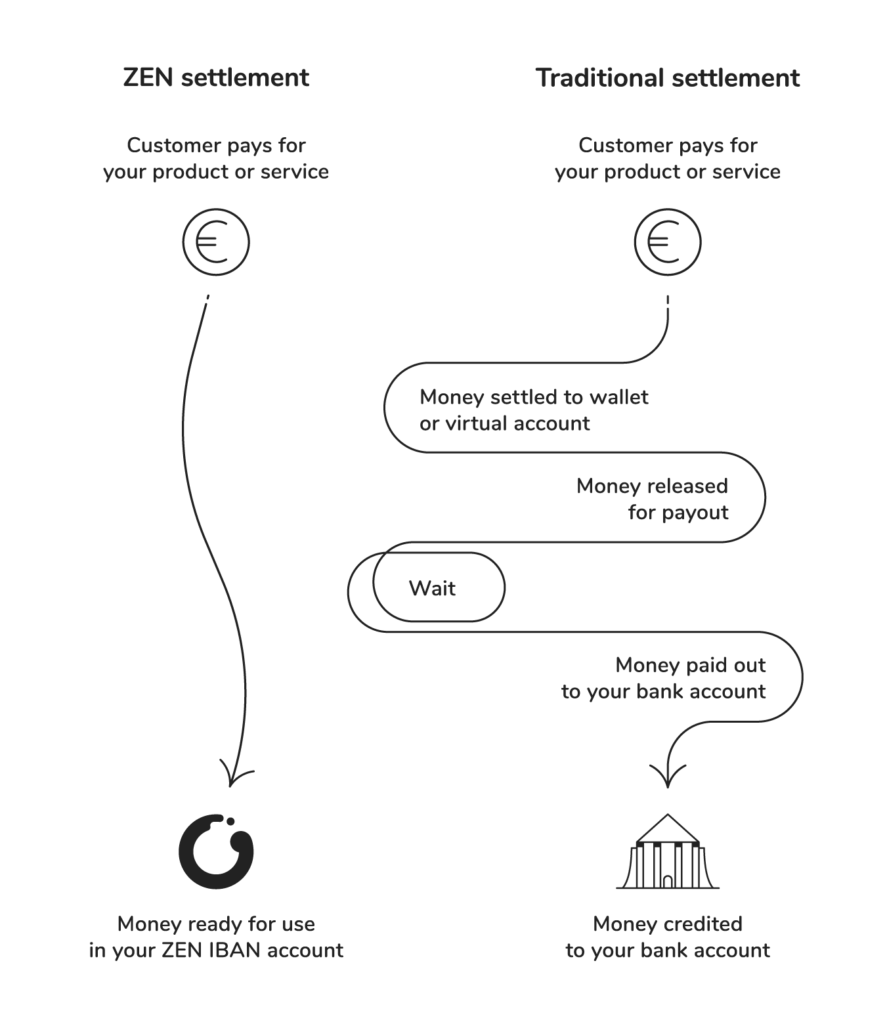

At ZEN, we offer a much more simplified transfer flow compared to traditional ones. You can skip the settlement payout part of payment processing and receive your money directly to your ZEN IBAN bank account.

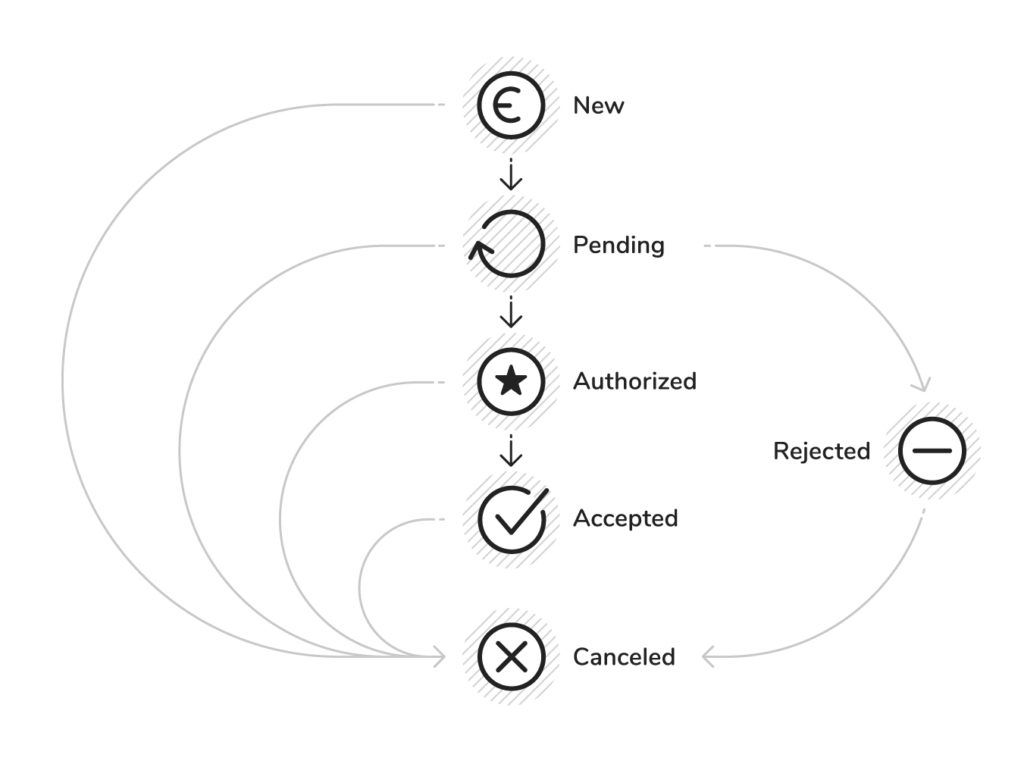

- ZEN payments begin with an authorization request. ZEN then directs users (or their payment data) to the selected payment operator.

- The payment is now PENDING. Once it is verified, you receive an IPN (Instant Payment Notification) that informs you of the payment’s status: AUTHORIZED, CANCELED, REJECTED, or ACCEPTED.

- If instant authorization is not available, the IPN may come with the PENDING status. If this happens, you should wait for the IPN with the final authorization status.

- Accepted transactions are settled to your ZEN IBAN account. Rejected transactions also contain a rejection reason code, which you can use to verify why the payment was not successfully processed.

Revenue streams

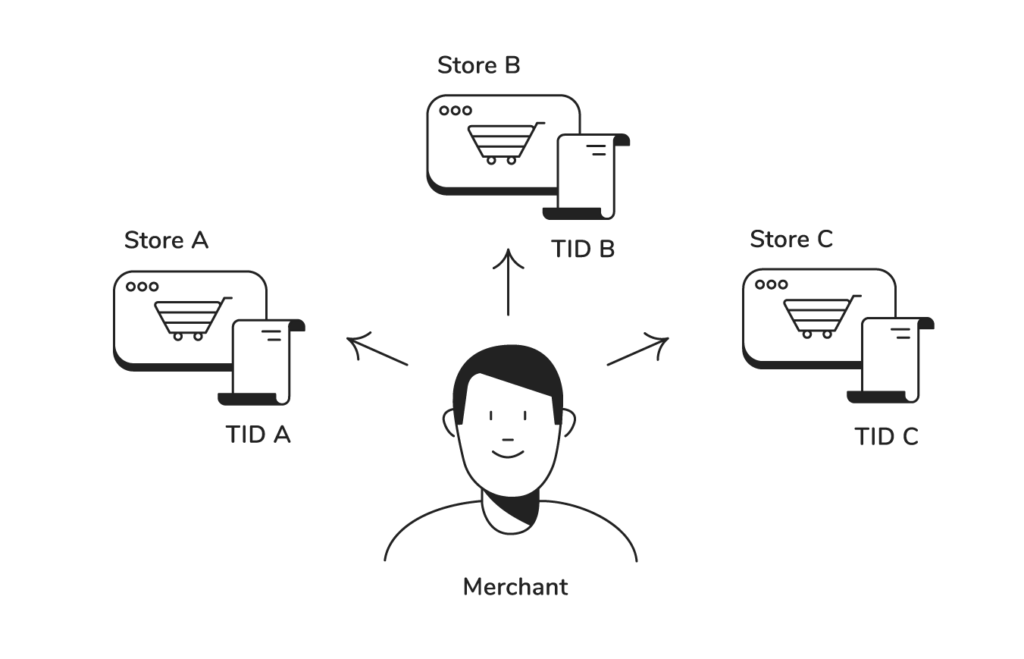

Revenue streams can be connected in a tree-like structure:

- The Merchant ID (MID) represents a legal entity acting as a merchant in a transaction.

- Each Merchant can generate a number of Shop IDs (SIDs) that represent the individual websites to which sales are made.

- Each SID is associated with a Terminal ID (TID), which contains information about the payment methods and currencies used by the stores.

- All transactions are handled at the Terminal level.